Post 17: Rate Cuts / Energy Check In / Currency Games

Post 17: Rate Cuts / Energy Check In / Currency Games

In the midst of a North American polar vortex the political climate is only just heating up in Iowa. The US appears resilient and new geopolitical scares occur once a month. 2024 will be a good year.

Rate Cuts?

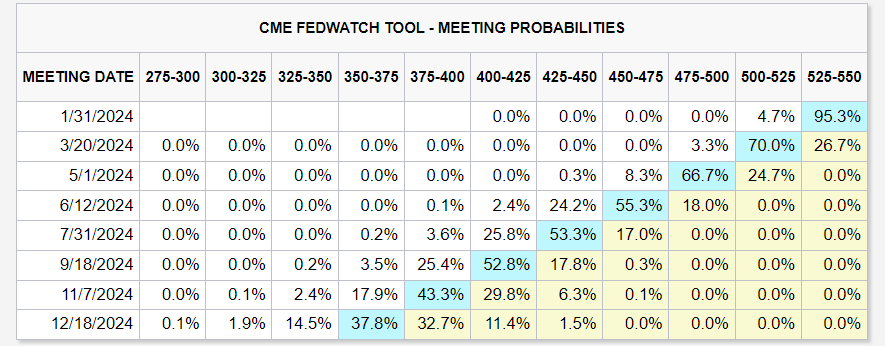

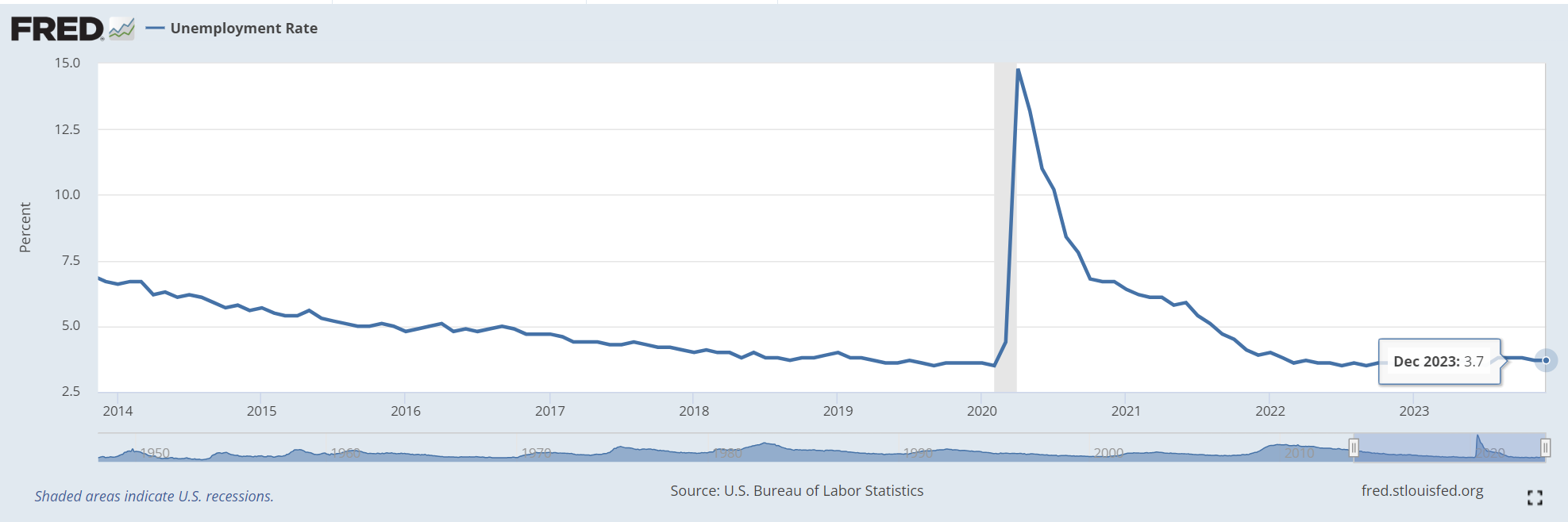

The market has been pricing in rate cuts in March, this is largely reflected in current market pricing, and describes the rally in equities in December (and late Nov). There is now a 73% chance of a cut in March, with the expectation of 25bp. The market expects +50% probability of 150bp in cuts by September. (see first 2 images). However, I see little incentive for the Fed to start cutting rates unless we run into trouble ahead. The market has proved resilient so far. There have been some sweeping layoffs, however this will help with corporate earnings and the unemployment rate is already very low. Those getting laid off in tech were likely from employee hoarding and those with technical skills will get hired quickly. Wages continue to increase and have showed no signs of slowing.

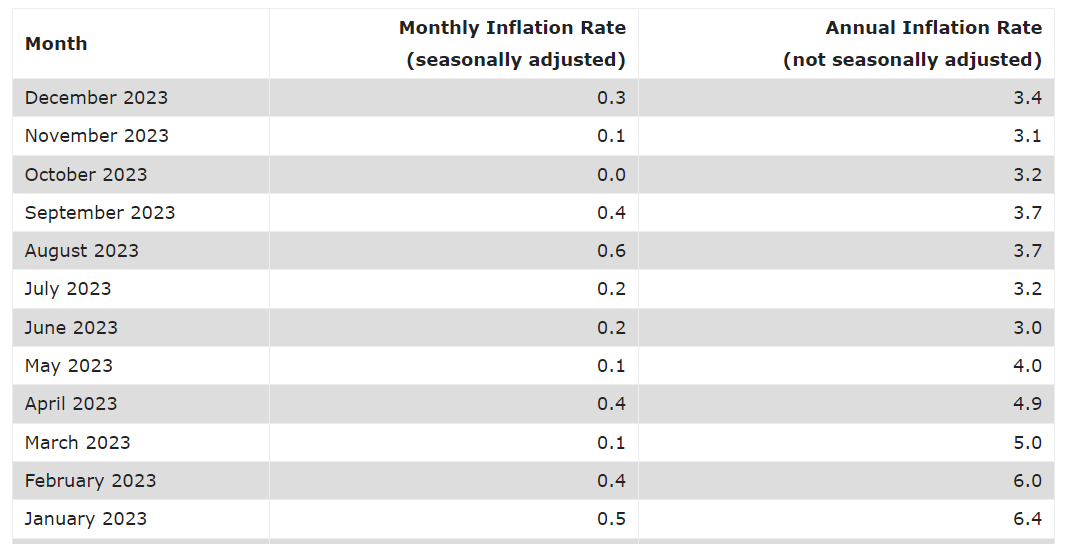

I believe the market will need to reconsider the likelihood of continued easing. The Fed has clearly not broken anything just yet, and they have not returned Inflation to their target rate. Without abandoning their mandate of 2% the Fed has no immediate need to start easing, financial conditions do no appear overly restrictive and they have shown progress against inflation over the last 2 years. If they were to start easing now it would be very likely that US inflation would be back with a vengeance.

I believe there is a trade here with the over anticipated rate cuts. My belief is that a slightly hawkish Fed at the next meeting will substantially decrease the odds of rate cuts through the year, push yields higher and suppressing/or reversing the bond rally.

It appears we may be in a reversal of the above trend but are far away from any positive correlation. A positive correlation would mean a rise in yields occurs as equity markets rally. This generally is a feature of a late-cycle economy, we have yet to experience any widening in credit spreads and growth has not deteriorated meaning we are not yet approaching the end of this cycle.

Energy Check In:

Before chatting oil I want to pat myself on the back. Yes, I got one thing right in 2023. (I got an unknown, but very high, number of things wrong, and luckily 1 right). The radioactive infinite energy cheat code of Uranium (that is a joke..) has continued its atmospheric rally since I last wrote about it on September 2023. To quote myself - “I think we are setting up for a further squeeze in the strategic resource. We don’t have any trades on with Uranium yet. But I am still long term bullish on the mineral.” We haven’t had a position in Uranium, but URA (GlobalxETF) would have been a +12% trade since September, miners like Cameco Corp (mostly Pure Play uranium) have done even better.

Now back to our main programming of Oil. There has been some relatively constant geopolitical shock occurring in the Middle East over the last 3 months. The more recent Houthis piracy have had little long term impact on price. OPEC+ production cuts are the only thing that has really moved oil for the past few months, and yet we remain trapped in a consolidation zone. In fact, oil has only continued its decline. I believe this was largely tied to sentiment and the demand outlook but there should be some upward momentum here soon with WTI back at the bottom of its range.

Currency Check In:

The USD has lost a lot of its strength against a a basket of key global currencies since the Oct high which ended a year long rally. With some progress being made against inflation in Europe (and the Ukraine war all but over), and no inflation at all in Japan its likely we see some ongoing strength in their economies. It will be interesting to see how easing policies in these regions, at a rate faster than the US, will impact FX.

US economic resilience speaks to the possibility of a strengthening dollar out of its recent weakness. We are bullish on the Aussie as we believe their will be higher demand for their primary industry goods as economies exit inflationary stages. They also appear to have improving relations with China which drives a lot of their exports. Aussie inflation continues to run higher than the US, but is decelerating much faster. If this trend continues we can expect some Aussie strength in 2024.